(Bloomberg) — Americans are increasingly likely to get turned down when they apply for credit, according to a new Federal Reserve survey that shows the combined impact of high interest rates and a cautious turn among the country’s lenders.

The rejection rate for loan applicants jumped to 21.8% in the 12 months through June, the highest level in five years, according to the latest edition of the Fed survey, which is published every four months. Overall credit applications declined to the lowest level since October 2020.

In the previous survey, published in February before the collapse of Silicon Valley Bank and other US lenders, the rejection rate was 17.3%. The increase since then has been broad-based across age groups, and highest among those with credit scores below 680.

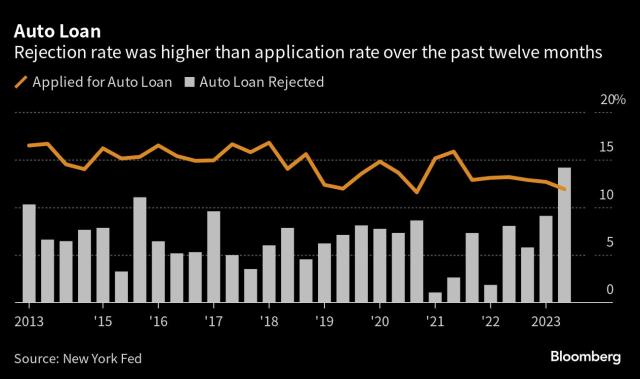

In auto loans, for the first time since the survey began in 2013 the rejection rate — which climbed to 14.2% from 9.1% — exceeded the application rate.

What’s more, almost one-third of auto-loan applicants expected that their loan would be rejected, a record high. There were also steep increases in reported expectations that requests for new mortgages, mortgage refinancing, or increases in credit-card limits would be turned down.